one-touch barrier binary option values

Abstract

We extend the binary options into barrier binary options and discuss the awarding of the optimal structure without a polish-fit condition in the option pricing. Nosotros outset review the existing piece of work for the knock-in options and present the chief results from the literature. Then nosotros show that the price part of a knock-in American binary pick can be expressed in terms of the price functions of simple bulwark options and American options. For the knock-out binary options, the smooth-fit property does not hold when we employ the local time-infinite formula on curves. By the properties of Brownian motion and convergence theorems, nosotros show how to summate the expectation of the local time. In the fiscal assay, we briefly compare the values of the American and European barrier binary options.

Share and Cite:

Gao, Chiliad. and Wei, Z. (2020) The Barrier Binary Options. Journal of Mathematical Finance, 10, 140-156. doi: 10.4236/jmf.2020.101010.

1. Introduction

Barrier options on stocks have been traded in the OTC (Over-The-Counter) market for more than 4 decades. The inexpensive cost of barrier options compared with other exotic options has contributed to their extensive use by investors in managing risks related to commodities, FX (Foreign Exchange) and interest rate exposures.

Barrier options accept the ordinary phone call or put pay-offs just the pay-offs are contingent on a second outcome. Standard calls and puts have pay-offs that depend on 1 market level: the strike price. Bulwark options depend on 2 market levels: the strike and the barrier. Barrier options come in 2 types: in options and out options. An in option or knock-in option simply pays off when the choice is in the coin with the barrier crossed earlier the maturity. When the stock cost crosses the barrier, the barrier option knocks in and becomes a regular option. If the stock price never passes the barrier, the selection is worthless no matter it is in the money or non. An out barrier option or knock-out pick pays off only if the choice is in the money and the barrier is never being crossed in the fourth dimension horizon. As long as the barrier is not being reached, the option remains a vanilla version. However, once the barrier is touched, the option becomes worthless immediately. More details about the barrier options are introduced in [i] and [2].

The apply of barrier options, binary options, and other path-dependent options has increased dramatically in recent years especially by large fiscal institutions for the purpose of hedging, investment and take a chance management. The pricing of European knock-in options in closed-form formulae has been addressed in a range of literature (meet [iii] [4] [5] and reference therein). In that location are two types of the knock-in selection: up-and-in and down-and-in. Any up-and-in call with strike above the barrier is equal to a standard call option since all stock movements leading to pay-offs are knock-in naturally. Similarly, whatever down-and-in put with strike below the barrier is worth the same as a standard put pick. An investor would buy knock-in selection if he believes the movements of the asset cost are rather volatile. Rubinstein and Reiner [vi] provided airtight form formulas for a wide variety of unmarried barrier options. Kunitomo and Ikeda [7] derived explicit probability formula for European double barrier options with curved boundaries equally the sum of infinite series. Geman and Yor [8] practical a probabilistic approach to derive the Laplace transform of the double barrier pick price. Haug [9] has presented analytic valuation formulas for American upwards-and-input and down-and-in telephone call options in terms of standard American options. It was extended by Dai and Kwok [10] to more types of American knock-in options in terms of integral representations. Jun and Ku [xi] derived a airtight-grade valuation formula for a digit barrier option with exponential random time and provided analytic valuation formulas of American partial barrier options in [12]. Hui [13] used the Black-Scholes environment and derived the belittling solution for knock-out binary option values. Gao, Huang and Subrahmanyam [14] proposed an early practice premium presentation for the American knock-out calls and puts in terms of the optimal free boundary.

There are many different types of bulwark binary options. It depends on: i) in or out; 2) up or down; 3) call or put; iv) cash-or-nothing or nugget-or-nothing. The European valuation was published by Rubinstein and Reiner [half-dozen]. However, the American version is not the combination of these options. This paper considers a broad diverseness of American barrier binary options and is organised every bit follows. In Department ii we introduce and set up the notation of the bulwark binary problem. In Section 3 nosotros formulate the knock-in binary options and briefly review the existing piece of work on knock-in options. In Section 4 we formulate the knock-out binary pick problem and give the value in the class of the early practise premium representation with a local time term. We bear a financial analysis in Section five and discuss the application of the barrier binary options in the electric current financial market.

2. Preliminaries

American feature entitles the pick heir-apparent the correct to exercise early. Regardless of the pay-off construction (cash-or-nothing and nugget-or-nothing), for a binary call option there are four basic types combined with barrier feature: up-in, up-out, down-in and downward-out. Consider an American (also known as "1-affect") upwards-in binary call. The value is worth the same as a standard binary call if the bulwark is below the strike since it naturally knocks-in to become the pay-off. On the other mitt, if the barrier is higher up the strike, the valuation turns into the aforementioned form of the standard with the strike price replaced past the barrier since we cannot practice if we just pass the strike and we volition immediately end if the option is knocked-in. Now permit us consider an upward-out call. Plainly, it is worthless for an upwardly-out telephone call if the bulwark is below the strike. Meanwhile, if the barrier is higher than the strike the stock will non hitting information technology since it stops one time it reaches the strike. For these reasons, it is more mathematically interesting to discuss the down-in or downward-out call and up-in or up-output.

Before introducing the American barrier binary options, we give a brief introduction of European bulwark binary options and some settings for this new kind of option.

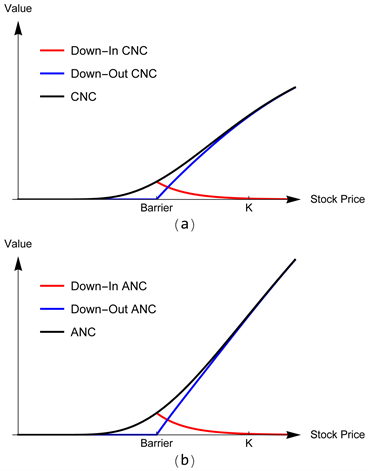

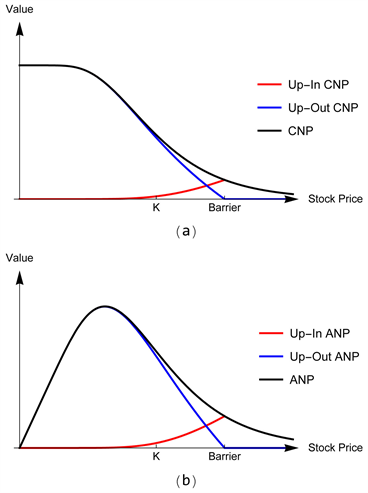

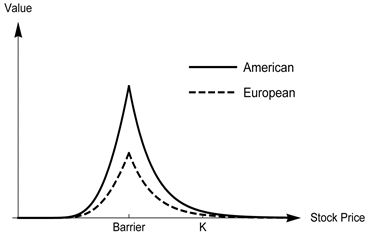

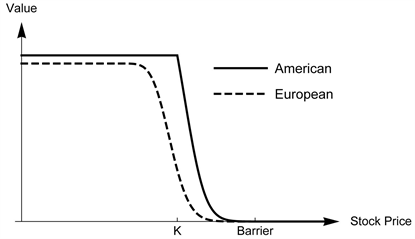

Figure 1 and Figure ii prove the value of eight kinds of European barrier binary options and the comparisons with corresponding binary choice values. All of the European barrier binary pick valuations are detailed in [half dozen]. Note that the payment is binary, therefore it is not an platonic hedging musical instrument so we do non analyse the Greeks in this paper and more applications of such options in financial market will exist addressed in Section v. Since we will study the American-style options, we simply consider the cases that barrier beneath the strike for the telephone call and bulwark above the strike for the put as reasons stated higher up. As we can see in Figure 1 and Figure ii, the barrier-version options in the blue or red curves are always worth less than the corresponding vanilla selection prices. For the binary call option in Effigy ane when the asset price is below the in-bulwark, the knock-in value is same as the standard price and the knock-out value is worthless. When the stock cost goes very loftier, the consequence of the barrier is intangible. The knock-intends to worth zippo and the knock-out value converges to the knock-less value. On the other mitt in Panel (a) of Effigy 2, the value of the binary put decreases with an increasing stock toll. As Panel (b) in Effigy 2 shows, the asset-or-nix put selection value showtime increases and so decreases as stock cost going large. At a lower stock cost, the issue of the bulwark for the knock-out value is trifle and the knock-in value tends to exist nil. When the stock price is above the barrier, the knock-out is worthless and the upward-in value gets the peak at the barrier. The figures also betoken the relationship

(2.ane)

Above all, barrier options create opportunities for investors with lower premiums than standard options with the same strike.

Figure ane. A calculator comparison of the values of the European barrier greenbacks-or-nothing call(CNC) and asset-or-nothing call(ANC) options for t given and stock-still.

Figure 2. A calculator comparison of the values of the European barrier cash-or-nothing put (CNP) and asset-or-nothing put (ANP) options for t given and fixed.

iii. The American Knock-In Binary Option

We start from the cash-or-zip option. At that place are four types for the cash-or-nothing option: up-and-in telephone call, down-and-in call, up-and-input and down-and-input. For the upward-and-in call, if the barrier is below the strike the option is worth the same as the American cash-or-zilch call since it will cross the barrier simultaneously to get the pay-off. On the other hand, if the barrier is above the strike the value of the option turns into the American cash-or-cipher call with the strike replaced by the bulwark level. Mathematically, the most interesting role of the greenbacks-or-nothing call option is downward-and-in call (also known every bit a downward-and-up pick). For the reason stated above, we only talk over upwards-and-input and down-and-in phone call in this section.

We assume that the up-in trigger clause entitles the option holder to receive a digital put option when the stock cost crosses the barrier level.

1) Consider the stock price X evolving every bit

(3.1)

with  nether P for any involvement rate

nether P for any involvement rate  and volatility

and volatility . Throughout

. Throughout  denotes the standard Brownian motion on a probability space

denotes the standard Brownian motion on a probability space . The arbitrage-gratis price of the American cash-or-null knock-in put selection at time

. The arbitrage-gratis price of the American cash-or-null knock-in put selection at time  is given by

is given by

(3.2)

(3.2)

where K is the strike price, L is the barrier level and  is the maximum of the stock toll process X. Recollect that the unique strong solution for (3.1) is given past

is the maximum of the stock toll process X. Recollect that the unique strong solution for (3.1) is given past

(3.iii)

(3.iii)

under . The process X is strong Markov with the minute generator given by

. The process X is strong Markov with the minute generator given by

(3.4)

(3.4)

We introduce a new process  which represents the process 10 stopped in one case information technology hits the barrier level L. Define

which represents the process 10 stopped in one case information technology hits the barrier level L. Define , where

, where  is the beginning striking time of the bulwark L equally

is the beginning striking time of the bulwark L equally

(3.v)

(3.v)

It means that nosotros do non demand to monitor the maximum procedure  since the procedure

since the procedure  behaves exactly the same as the process X for any time

behaves exactly the same as the process X for any time  and most of the properties of 10 follow naturally for

and most of the properties of 10 follow naturally for .

.

2) Standard Markovian arguments lead to the following complimentary-boundary problem

(3.half-dozen)

(3.half-dozen)

(3.vii)

(3.vii)

(3.8)

(3.8)

(three.9)

(three.9)

(iii.10)

(iii.10)

where the continuation gear up is expressed as

(three.11)

(three.11)

and the stopping prepare is given by

(3.12)

(3.12)

and the optimal stopping time is given by

(3.13)

(3.13)

The proof is easy to nourish past applying the definition of optimal stopping fourth dimension.

iii) Summarising the preceding facts, we can at present utilize the approach used in [ten] and [15] to obtain a representation for the price of the American knock-in binary option as follows:

(iii.14)

(iii.14)

for  and

and , where

, where  is the probability density function of the first hitting time of the process (three.1) to the level Fifty. The density office is given past (come across e.g. [sixteen])

is the probability density function of the first hitting time of the process (three.1) to the level Fifty. The density office is given past (come across e.g. [sixteen])

(three.15)

(three.15)

for  and

and , where

, where  is the standard normal density function given by

is the standard normal density function given by  for

for . Therefore, the expression for the

. Therefore, the expression for the

arbitrage-free cost is given by (iii.14) and can be solved by inserting the price of the American cash-or-aught put option.

The value of the American cash-or-zilch put option is given past [half dozen]

(iii.xvi)

(iii.xvi)

The other three types of binary options: cash-or-goose egg call, asset-or-nothing phone call and put follow the aforementioned pricing process and their American values can be referred in [half-dozen].

4. The American Knock-Out Binary Options

four.1. The American Knock-Out Cash-Or-Nothing Options

1) Consider the stock price 10 evolving every bit

(4.1)

(4.1)

with  under P for any interest rate

under P for any interest rate  and volatility

and volatility . Throughout

. Throughout  denotes the standard Brownian movement on a probability space

denotes the standard Brownian movement on a probability space . The arbitrage-free price of the American upwardly-out greenbacks-or-naught put selection at time

. The arbitrage-free price of the American upwardly-out greenbacks-or-naught put selection at time  is given by

is given by

(4.two)

(4.two)

where 1000 is the strike price, Fifty is the bulwark level and  is the maximum of the stock price process X. Recall that the unique strong solution for (4.1) is given by

is the maximum of the stock price process X. Recall that the unique strong solution for (4.1) is given by

(iv.3)

(iv.3)

under . The process X is strong Markov with the infinitesimal generator given by

. The process X is strong Markov with the infinitesimal generator given by

(4.iv)

(4.iv)

We innovate a new procedure  which represents the process X stopped in one case it hits the barrier level L. Define

which represents the process X stopped in one case it hits the barrier level L. Define , where

, where  is the start hitting time of the barrier Fifty:

is the start hitting time of the barrier Fifty:

(four.five)

(four.five)

It ways that we exercise not need to monitor the maximum procedure  since the process

since the process  behaves exactly the aforementioned every bit the procedure X for whatever time

behaves exactly the aforementioned every bit the procedure X for whatever time  and nearly of the properties of X follow naturally for

and nearly of the properties of X follow naturally for .

.

2) Let us determine the structure of the optimal stopping trouble (iv.2). Standard Markovian arguments lead to the following gratis-boundary problem (see [17])

(four.6)

(four.6)

(iv.7)

(iv.7)

(4.8)

(4.8)

(4.nine)

(4.nine)

(4.10)

(4.10)

where the continuation gear up is expressed as

(4.11)

(4.11)

the stopping ready is given by

(iv.12)

(iv.12)

and the optimal stopping fourth dimension is given by

(4.13)

(4.13)

denoting the first time the stock cost is equal to K before the stock price is equal to L. We volition prove that One thousand is the optimal purlieus and  is optimal for (4.two) below.

is optimal for (4.two) below.

3) Nosotros will evidence that (4.13) is optimal for (4.two). The fact that the value office (iv.2) is a discounted price indicates that the larger  is, the less value nosotros will get. As to the payoff, it is either £1 or nothing. Therefore, the optimal stopping time is just the very starting time time that the stock price hits G, which is (four.13). To prove this, nosotros ascertain

is, the less value nosotros will get. As to the payoff, it is either £1 or nothing. Therefore, the optimal stopping time is just the very starting time time that the stock price hits G, which is (four.13). To prove this, nosotros ascertain  as whatsoever stopping fourth dimension. Nosotros demand to show that

as whatsoever stopping fourth dimension. Nosotros demand to show that

(4.14)

(4.14)

Actually,

(4.15)

(4.15)

On the other hand,

(4.sixteen)

(4.sixteen)

Hence we conclude that  is optimal in (4.2).

is optimal in (4.2).

4) Based on the optimal stopping time (4.13), a direct solution for (4.ii) tin exist expressed equally

(4.17)

(4.17)

For the geometric Brownian movement the density  is known in closed form (cf. ( [16], Page 622):

is known in closed form (cf. ( [16], Page 622):

(4.18)

(4.18)

for , where

, where  is given by (cf. [16])

is given by (cf. [16])

(4.19)

(4.19)

for . The result is straightforward

. The result is straightforward

(four.20)

(four.20)

for . The value function concerns with the convergence due to the sum of an infinite series. More precisely we volition apply the optimal stopping theory to value (four.2) and get a better result. Nevertheless, the result from (4.twenty) indicates some backdrop of the pricing (four.ii). It is piece of cake to verify that local time-infinite formula is applicative to our problem (iv.2).

. The value function concerns with the convergence due to the sum of an infinite series. More precisely we volition apply the optimal stopping theory to value (four.2) and get a better result. Nevertheless, the result from (4.twenty) indicates some backdrop of the pricing (four.ii). It is piece of cake to verify that local time-infinite formula is applicative to our problem (iv.2).

5) To get the solution to the optimal stopping problem (4.two), apply Ito'southward formula to  and get

and get

(4.21)

(4.21)

where the office  is defined by

is defined by

(4.22)

(4.22)

is given by

is given by

(4.23)

(4.23)

and  refers to integration with respect to the continuous increasing role

refers to integration with respect to the continuous increasing role , and

, and  is a continuous local martingale for

is a continuous local martingale for  with

with .

.

The martingale term vanishes when taking E on both sides. From the optional sampling theorem we get

(iv.24)

(iv.24)

for all stopping times  of X with values in

of X with values in  with

with  and

and  given and fixed. Replacing due south by

given and fixed. Replacing due south by  in (4.24), nosotros get

in (4.24), nosotros get

(four.25)

(four.25)

for all , where

, where  and

and  for

for . We obtain the following early exercise premium representation of the value function

. We obtain the following early exercise premium representation of the value function

(4.26)

(4.26)

The first term on the RHS is the arbitrage-free price of the European knock-out cash-or-naught put option  at the bespeak

at the bespeak  and can be written explicitly as (run across [vi])

and can be written explicitly as (run across [vi])

(4.27)

(4.27)

We write

(4.28)

(4.28)

Call up that the joint density office of geometric Brownian motion and its maximum  under P with

under P with  is given by (see [16])

is given by (see [16])

(iv.29)

(iv.29)

for  with

with .

.

6) Nosotros will discuss the calculation about the local-time term  (see [18] and reference therein). Notation that

(see [18] and reference therein). Notation that

(4.30)

(4.30)

From the definition of local time  , in that location exists a sequence

, in that location exists a sequence  such that

such that  and

and  -

- . Using Dominated Convergence Theorem, we get

. Using Dominated Convergence Theorem, we get

(4.31)

(4.31)

The second step is attained by Fubini's Theorem and Dominated Convergence Theorem. By the definition of derivative, the last stride in (4.31) equals

(4.32)

(4.32)

The density function  is given by

is given by

(four.33)

(four.33)

where  is the density function for standard normal distribution. Therefore, (4.30) can be expressed as

is the density function for standard normal distribution. Therefore, (4.30) can be expressed as

(4.34)

(4.34)

Substituting the effect (four.34) into (4.26), nosotros get the early exercise premium (EEP) representation for the American knock-out cash-or-zero put pick

(4.35)

(4.35)

where the first and second terms are defined in (4.27) and (iv.28).

The main result of the present subsection may now be stated as follows. Beneath, we will make employ of the post-obit function

(4.36)

(4.36)

for all  and

and .

.

Theorem 1. The arbitrage-free price of the American knock-out cash-or-nothing put option follows the early-exercise premium representation

(4.37)

(4.37)

for all , where the first term is the arbitrage-free price of the European knock-out cash-or-nothing put option and the second and third terms are the early-exercise premium.

, where the first term is the arbitrage-free price of the European knock-out cash-or-nothing put option and the second and third terms are the early-exercise premium.

The proof is straightforward following the points 4, 5 and half dozen stated higher up. Note that our trouble is based on the stopped process  instead of the original process X and that the value of

instead of the original process X and that the value of  in (iv.37) needs to be estimated by finite difference method otherwise we tin not go the value

in (iv.37) needs to be estimated by finite difference method otherwise we tin not go the value .

.

The cash-or-nothing call option tin can be handled in a similar way. The dissimilar part is the European value function in (4.27). The arbitrage-free toll of the European downward-out cash-or-nothing call option  at the bespeak

at the bespeak  is given by (see [half dozen])

is given by (see [half dozen])

(4.38)

(4.38)

4.2. The American Knock-Out Asset-Or-Nothing Options

The arbitrage-free toll of the European knock-out asset-or-nothing choice  at the betoken

at the betoken  can exist written explicitly as (encounter [vi])

can exist written explicitly as (encounter [vi])

(iv.39)

(iv.39)

(4.40)

(4.40)

where  represents the value for the European down-out asset-or-zero call (ANC) option and

represents the value for the European down-out asset-or-zero call (ANC) option and  for the upwards-out put.

for the upwards-out put.

Theorem ii. The arbitrage-complimentary price of the American knock-out asset-or-null selection follows the early-practice premium representation

(4.41)

(4.41)

for all , and

, and

(4.42)

(4.42)

for all , where the offset term is the arbitrage-free cost of the European knock-out asset-or-nothing option and the 2d term is the early-exercise premium.

, where the offset term is the arbitrage-free cost of the European knock-out asset-or-nothing option and the 2d term is the early-exercise premium.

Proof. The proof is coordinating to that of Theorem 1. Back to (four.22), it is easy to verify that the value of H vanishes since  in the stopping set. At that place are only two terms in (iv.26).

in the stopping set. At that place are only two terms in (iv.26).

five. Fiscal Analysis of the American Bulwark Binary Options

The payment of the American barrier binary options is binary, and so they are not platonic hedging instruments. Instead, they are platonic investment products. It is pop to utilise structured accrual range notes in the financial markets. Such notes are related to foreign exchanges, equities or commodities. For instance, in a daily accrual USD-BRP exchange rate range note, information technology pays a fixed daily accrual interest if the substitution rate remains within a certain range.

By and large, an investor buying a barrier selection is seeking for more adventure than that of a vanilla option since the barrier options can exist stopped or "knocked-out" at whatsoever time prior to maturity or never start or "knock-in" due to not striking the bulwark. Basic reasons to purchase bulwark options rather than standard options include a amend expectation of the future behaviour of the market, hedging needs and lower premiums. In the liquid market, traders value options by calculating the expected value of the pay-offs based on all stock scenarios. It means to some extent we pay for the volatility around the forward price. Withal, barrier options eliminate paying for the impossible scenarios from our indicate of view. On the other paw, nosotros tin improve our render by selling a bulwark option that pays off based on scenarios we think of little probability. Permit united states of america imagine that the 1-yr forward price of the stock is 110 and the spot cost is 100. We believe that the market place is very likely to ascent and if it drops below 95, it will reject farther. We tin buy a down-and-out phone call option with strike price 110 and the barrier level 95. At whatever time, if the stock falls below 95, the option is knocked-out. In this way, we practise not pay for the scenario that the stock price drops firstly then goes upwardly again. This reduces the premium. For the hedgers, bulwark options meet their needs more closely. Suppose we own a stock with spot 100 and decide to sell it at 105. We as well want to go protected if the stock price falls beneath 95. Nosotros can buy a put option struck at 95 to hedge it merely it is more inexpensive to buy an up-an-out put with a strike price 95 and bulwark 105. Once the stock price rises to 105 when we tin sell it and this put disappears simultaneously.

The relationship between knock-in choice, knock-out option and knock-less option (standard choice) of the same type (phone call or put) with the same expiration date, strike and bulwark level can be expressed every bit

(v.i)

(v.i)

This relationship only holds for the European barrier options. It has not been obtained for the American version when we get the American values from the sections above.

We plot the value of the American barrier binary options using the free-boundary construction in the above sections. Note that the value of  in Equations (four.37), (4.41) and (4.42) separately is estimated past finite divergence method (run across [19]).

in Equations (four.37), (4.41) and (4.42) separately is estimated past finite divergence method (run across [19]).

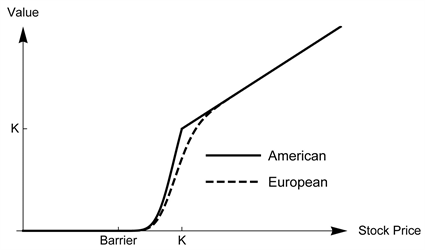

The American value curves in Figure 3 and Figure 4 are simulated from (xv) by inserting different American binary option values. Figure iii shows that the value of the American downwardly-in cash-or-goose egg call options (nugget-or-nothing call pick follows a similar bend) increases with stock toll  before the in barrier and then decreases due to the incertitude of knock-in. Figure 4 shows the value of the American up-in greenbacks-or-nothing put option (asset-or-nothing put is similar ). Every bit we tin can see before the barrier, the option value is increasing and gets its superlative at the barrier. And then the value goes down as the stock price continues to go up after the barrier level. Generally, the toll of the American version options is larger than the European version.

before the in barrier and then decreases due to the incertitude of knock-in. Figure 4 shows the value of the American up-in greenbacks-or-nothing put option (asset-or-nothing put is similar ). Every bit we tin can see before the barrier, the option value is increasing and gets its superlative at the barrier. And then the value goes down as the stock price continues to go up after the barrier level. Generally, the toll of the American version options is larger than the European version.

Figures 5-8 show the values for the knock-out binary options. Figure five illustrates that the value of the upwardly-out cash-or-zippo put choice is a decreasing function of the stock price below the bulwark. Still, in Figure half-dozen the up-out asset-or-zilch put first goes up and and then down to the barrier. We tin see the value of the down-out greenbacks-or-nothing call option in Figure seven is strictly increasing as the asset price higher up the barrier. The asset-or-nothing call value in Figure viii is also in the similar situation but with different corporeality of payoff size. All of the out figures show that the smooth-fit status is not satisfied at the stopping boundary K.

Figure three. A reckoner comparison for the values of the European and the American down-in cash-or-nothing call options with parameters  and

and .

.

Figure 4. A computer comparison for the values of the European and the American up-in cash-or-nothing put options with parameters  and

and .

.

Effigy 5. A calculator comparison for the values of the European and the American up-out greenbacks-or-cipher put options with parameters  and

and .

.

Figure 6. A computer comparison for the values of the European and the American up-out asset-or-nothing put options with parameters  and

and .

.

Effigy 7. A reckoner comparison for the values of the European and the American down-out cash-or-cipher telephone call options with parameters  and

and .

.

The results of this newspaper also concur for an underlying asset with dividend structure. With pocket-size modifications, the formulas developed hither tin can be applied to handle those issues.

Figure eight. A reckoner comparing for the values of the European and the American down-out nugget-or-nothing telephone call options with parameters  and

and .

.

Acknowledgements

The authors are grateful to Goran Peskir, Yerkin Kitapbayev and Shi Qiu for the informative discussions.

Conflicts of Interest

The authors declare no conflicts of involvement.

References

| [1] | Derman, Eastward. and Kani, I. (1996) The Ins and Outs of Barrier Options: Part 1. Derivatives Quarterly, 3, 55-67. |

| [ii] | Derman, E. and Kani, I. (1997) The Ins and Outs of Barrier Options: Function two. Derivatives Quarterly, iii, 73-lxxx. |

| [3] | Haug, E.M. (2007) The Complete Guide to Selection Pricing Formulas. McGraw-Hill Companies, New York. |

| [4] | Merton, R.C. (1973) Theory of Rational Option Pricing. The Bell Journal of Economic science and Management Science, 4, 141-183. https://doi.org/10.2307/3003143 |

| [5] | Rich, D.R. (1994) The Mathematical Foundations of Barrier Option-Pricing Theory. Advances in Futures and Options Research: A Enquiry Annual, 7, 267-311. |

| [half dozen] | Rubinstein, M. and Reiner, Due east. (1991) Unscrambling the Binary Code. Take a chance Magazine, 4, 20. |

| [7] | Kunitomo, North. and Ikeda, Chiliad. (1992) Pricing Options with Curved Boundaries. Mathematical Finance, two, 275-298. https://doi.org/10.1111/j.1467-9965.1992.tb00033.x |

| [eight] | Geman, H. and Yor, Thousand. (1996) Pricing and Hedging Double-Barrier Options: A Probabilistic Approach. Mathematical Finance, 6, 365-378. https://doi.org/10.1111/j.1467-9965.1996.tb00122.x |

| [9] | Haug, Due east.G. (2001) Closed Course Valuation of American Barrier Options. International Journal of Theoretical and Applied Finance, 4, 355-359. https://doi.org/10.1142/S0219024901001012 |

| [10] | Dai, K. and Kwok, Y.One thousand. (2004) Knock-in American Options. Journal of Futures Markets, 24, 179-192. https://doi.org/10.1002/fut.10101 |

| [11] | Jun, D. and Ku, H. (2012) Digital Barrier Option Contract with Exponential Random Fourth dimension. IMA Journal of Applied Mathematics, 78, 1147-1155. https://doi.org/10.1093/imamat/hxs013 |

| [12] | Jun, D. and Ku, H. (2013) Valuation of American Partial Barrier Options. Review of Derivatives Inquiry, 16, 167-191. https://doi.org/ten.1007/s11147-012-9081-1 |

| [xiii] | Hui, C.H. (1996) Ane-Affect Double Barrier Binary Choice Values. Practical Fiscal Economics, half dozen, 343-346. https://doi.org/10.1080/096031096334141 |

| [14] | Gao, B., Huang, J.Z. and Subrahmanyam, M. (2000) The Valuation of American Barrier Options Using the Decomposition Technique. Journal of Economic Dynamics and Command, 24, 1783-1827. https://doi.org/x.1016/S0165-1889(99)00093-vii |

| [15] | Aitsahlia, F., Imhof, L. and Lai, T.50. (2004) Pricing and Hedging of American Knock-in Options. The Journal of Derivatives, eleven, 44-50. https://doi.org/10.3905/jod.2004.391034 |

| [16] | Borodin, A.N. and Salminen, P. (2002) Handbook of Brownian Motion: Facts and Formulae. Springer, Berlin. https://doi.org/ten.1007/978-3-0348-8163-0 |

| [17] | Peskir, G. and Shiryaev, A. (2006) Optimal Stopping and Complimentary-Boundary Problems. Birkhäuser, Basel. |

| [18] | Peskir, 1000. (2005) A Alter-of-Variable Formula with Local Time on Curves. Journal of Theoretical Probability, 18, 499-535. https://doi.org/10.1007/s10959-005-3517-6 |

| [nineteen] | Qiu, Due south. (2016) Early Exercise Options with Two Costless Boundaries. PhD Thesis, The Academy of Manchester, Manchester. |

Source: https://www.scirp.org/journal/paperinformation.aspx?paperid=98476

Posted by: candelariotrest1944.blogspot.com

0 Response to "one-touch barrier binary option values"

Post a Comment